This is NOT a how-to-become-a-full-time-blogger post.

I’m not a full-time blogger. I don’t currently make a full-time income. As of this writing, I’ve been blogging for about 15 months, and while I make enough money to afford a new car every year (new to me, anyway), I’m nowhere near full-time status!

But I’ve spent a lot of time analyzing just how much money I need to make in order to leave my job and go full-time. And it’s not as simple as saying, “When my blog revenue equals my salary, I’ll leave.”

I just want to share some of my thoughts. If you’re planning for D-Day like I am, maybe my strategies can help you!

What Is the Seasonality of Your Niche?

My salary wages arrive in my bank account every two weeks, without fail. But my blogging income varies from month to month, season to season, year to year.

Most niches are seasonal. Real estate peaks in the spring, turkeys in Thanksgiving, and health insurance in the late fall.

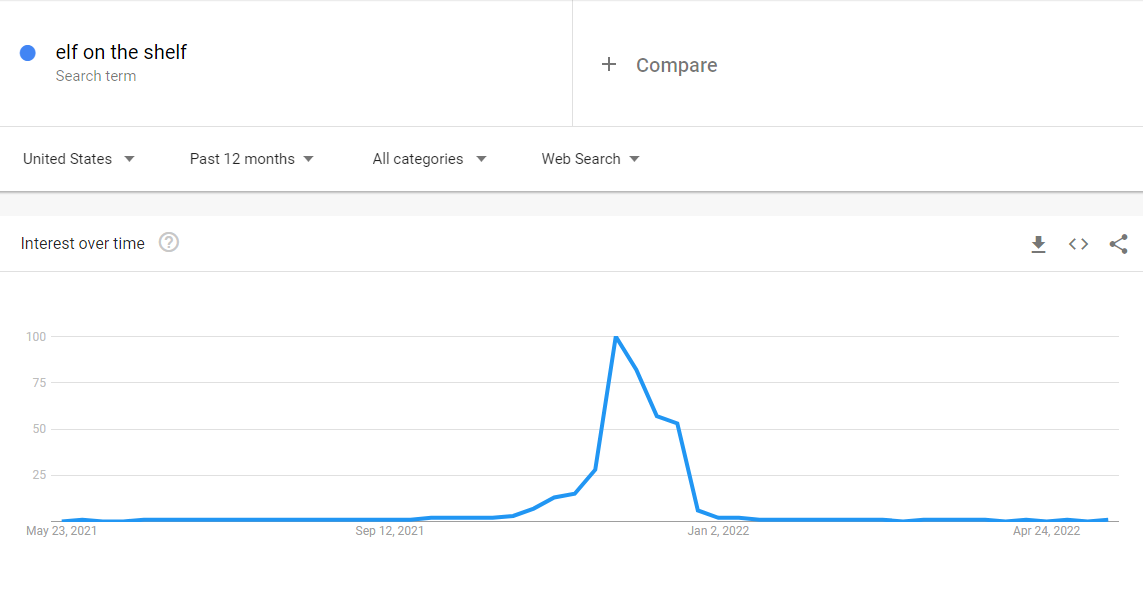

Here’s a picture from Google Trends about a super-seasonal topic: “Elf on The Shelf.”

If you make most of your money from affiliate Elf on the Shelf book sales, summer is gonna be a lean season for you!

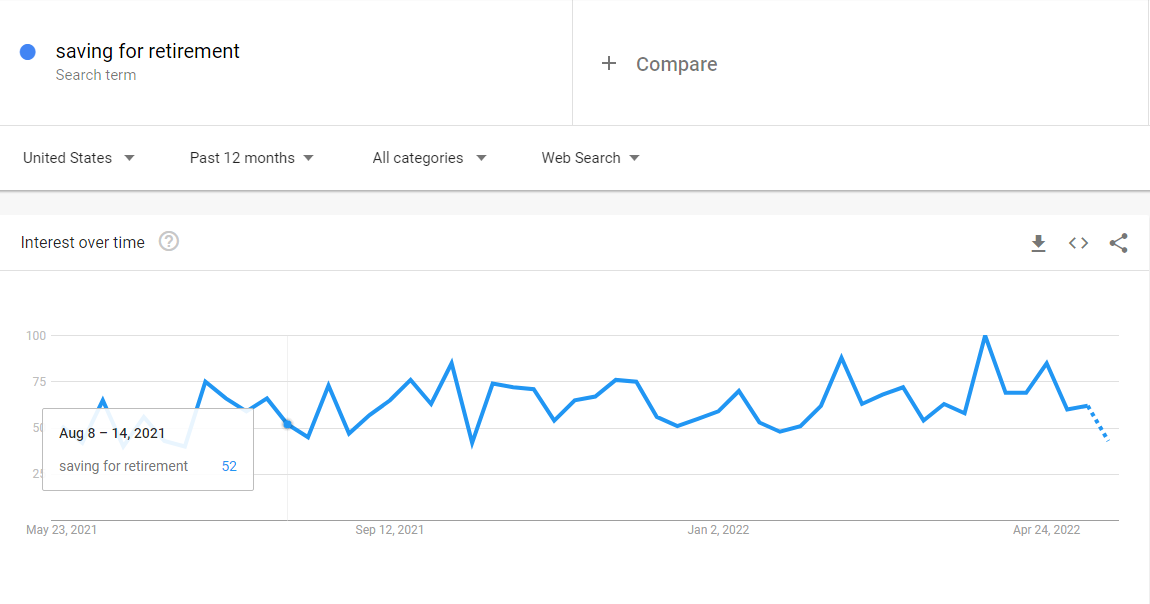

On the other hand, look at the search query: “Saving for retirement.” There’s a minor uptick during tax season, but other than that, it’s consistent across the year. This is a niche that will fluctuate with the state of the economy more than the time of year.

All niches have seasonality, whether it’s the calendar year, sports playoffs, state of the economy, or voting years.

Before you quit your job to blog full-time, you need to know:

- What are my seasonality factors?

- What’s the difference in average income between high and low seasons?

And plan accordingly. You don’t want to be living paycheck-to-paycheck during the off-season! And ask yourself – do you have the financial fortitude to save during the feast to prepare for the famine?

What’s Your Risk Tolerance?

This is a similar question to the first one … but basically I’m asking how much can you afford to lose?

Say an algorithm unfairly strikes your website. Traffic is down 25%. What happens?

Another way of thinking about this question is what’s your margin? How much can you afford to lose before you’re scouring Indeed job postings and contemplating selling the house?

Let’s put a number on it.

- Could you afford to lose 10% of your blog revenue? If not, then you’re risk-averse, and likely not ready to take the plunge into full-time blogging.

- Could you afford to lose 20% of your blog revenue? If not, then you can only accept low risk over the short term. Losing any more than a handful of top-ranked pages could put you under.

- Could you afford to lose 30% of your blog revenue? If not, then you can probably accept moderate risk without compromising your lifestyle.

- Can you afford to lose 50% or more of your income? If yes, then why are you reading this article? Go full-time, now!

What Are Your Material Lifestyle Requirements?

When I think about my risk tolerance, I think about my minimum material lifestyle requirements. For instance, let’s say I’m a celebrity-in-the-making. I buy Ray-Bans, drive BMWs, and wear Rolexes. If that’s the minimum lifestyle I’m willing to accept, then I better start writing 10 blog posts a day!

But if I’m willing to accept a less materialistic lifestyle, then my margin increases. If I drive used cars, set the air conditioning to 77 degrees, and make my own coffee, then even if I lose 25% of my revenue, I can still make ends meet – and maintain that lifestyle.

Having a family can really complicate this. But you need to sit down and honestly discuss your wants/needs with your spouse. You both need to be on the same page about what’s an acceptable material lifestyle before you commit to full-time self-employment – and you both need to agree on what would trigger a mandatory return to gainful employment! Otherwise, future financial losses can brew feelings of resentment.

Here’s a little table I made that helps me define my income requirements. These numbers are pulled somewhat from U.S. Census Data, but they’re also limited by my own experiences. I live in a rural area; if you live in a Big City, add 20% to everything.

Oh, and pay attention to the headers! This table references blog profit, not revenue. You need to subtract expenses, like overhead and contractor fees, from your revenue to calculate profit.

If you don’t know your expenses (hosting, marketing, software, computers, etc.) off the top of your head, then just estimate 10% of your revenue goes to expenses.

| Blog Monthly PROFIT | Equivalent Hourly Wage | Equivalent Annual Wage | Comparable To | Notes |

| 0 – $1,666 | $7.25-$10 | <$20,000/year | Minimum wage employment | unskilled labor | Hmm … better keep it as a side hustle? |

| $1,666 – $2,500 | $10-$15 | $20,000 – $30,000 | Entry-level skilled labor | Likely doesn’t have enough margin for minimum lifestyle nor profit for lost employment benefits. |

| $2,500 – $3,333 | $15-$20 | $30,000 – $40,000 | Moderate-level skilled labor | low-level professional career | The median American personal income is about $35,000 a year. Median blogger income is less, just under $30,000. You’re doin’ alright! – but a severe setback could be catastrophic. |

| $3,333 – $4,166 | $20 – $25 | $40,000 – $50,000 | High-level skilled labor | Moderate-level professional career | Good income, but limited lifestyle options. Not likely enough to support a family on a single income. |

| $4,166 – $5,833 | $25 – $35 | $50,000 – $70,000 | Very high skilled labor | high professional career | Very good income. Could support some families on a single income on simple lifestyles. |

| $5,833 – $8,333 | $35 – $50 | $70,000 – $100,000 | Excellent skilled labor | very high professional career | Excellent income! Will make your friends’ eyes bug out when you say, “I’m a full-time blogger, too.” |

| $8,333+ | $50+ | $100,000+ | Excellent for anyone! | Tell that engineer or lawyer to go suck an egg! Likely less than 1% of bloggers make more than 100k a year. And unlike a doctor, you don’t have $300,000 in medical student loans to pay off. |

For my part, my material lifestyle requirements are moderate (I drive a Honda, not a Mercedes – but also not a Scion). But I would like to make enough money to support a family on a single-family income, and I’d like to be able to comfortably survive a 25% drop in income. Put those two things together, and that’s why I’m aiming to make six figures.

What Is the Basis of Your Revenue?

As bloggers, we sometimes forget that page views are worthless. You can’t eat, trade, or steal a page view. Somewhere along the line, someone has to fork over real money in order for us to generate any revenue!

So what’s the basis of your revenue? Phrased another way, what are your income streams? Or perhaps simplest of all, how do you make money?

- If you make money through selling advertising inventory, what could jeopardize your clicks? Are you at risk of being kicked off AdSense for violations or booted out of Mediavine if your traffic plummets after an algorithm update?

- If you make money through affiliate commissions, how confident are you in your commission rates? May I remind you of the Amazon Armageddon in spring 2020?

- If you make money selling printables or digital downloads, how easily can that content be plagiarized? Are you at the mercy of another platform, or do you have enough organic exposure to weather chaos on social media platforms?

- If you make money through members-only content, what could cut your membership rates? What could bump up your customer acquisition costs or increase membership turnover?

What’s Your Adjusted Net Compensation?

As a blogger, you get no health insurance, no matching 401(k), no paid vacation, no paid holidays, no free donuts, nothin’. You get cash. Do with it what you will.

If you’re thinking about leaving your full-time job to become a professional blogger, you need to know how much you actually earn right now. That includes wages and benefits!

Here’s a short list of compensation benefits you might be receiving (or could receive) from your employment:

- Wages and bonuses

- Profit-sharing payouts

- 401(k)

- Health insurance

- Dental insurance

- Life insurance

- Paid time off

- Sick time off

- Paid medical leave

- Health savings accounts

- Adoption assistance

- Education and tuition assistance

- Stock options

Each of those benefits has a dollar value. And it’s not a small amount. It’s not uncommon for 20, 30, even 40% of a job’s compensation to be tied up in the benefits package!

This is where you might need to enlist the help of an accountant or financial planner. Don’t ask me. But you need to know the evaluation of your benefits package before you walk away from it.

You are allowed to subtract the costs of your current employment, as well. If you drive 45 minutes to work every day, subtract the costs of fuel and car maintenance from the benefits.

And don’t forget about those pesky opportunity costs. Losing $500 a month in IRA savings could mean hundreds of thousands of dollars of lost investment in the stock market over time!

But now I’m starting to sound like a tax accountant. You get the idea. Count the costs!

***

At some point, in the hopefully-not-too-distant future, I will release Part 2 of this blog post: How to Become a Full-Time Blogger!

But for now, I’ll keep cranking away, 1,000 words at a time.